Egypt has made strides in harmonizing its financial and regulatory frameworks to achieve two key objectives simultaneously: promoting a greener economy and executing an ambitious development strategy. However, tremendous challenges lie ahead for Egypt, including monetary and fiscal imbalances, overreliance on external development banks and slow progress in utilizing revenue-generating resources related to climate initiatives. To address these challenges, Egypt should lean in further to accelerate the green transition in the energy sector by increasing investments in renewables, aligning its taxes and other financial policy frameworks with its green objectives and designing a mature taxonomy system to add more clarity and transparency to banks and other financial institutions.

A fast track to sustainability

A shortfall in available financing, a relative lack of progress on economic reform and the prioritisation of social objectives have reduced the speed of Egypt’s transition. Yet, there are indications that these hurdles will not impede Egypt’s sustainability plans in the longer term.

Egypt’s government has shifted its perspective from seeing environmental considerations as obstacles to investment to recognizing them as valuable opportunities. For instance, in 2019, the National Climate Change Council, headed by the prime minister, was entrusted with climate responsibilities in preparation for COP 27, which took place in Sharm el-Sheikh in 2022, indicating support at the highest levels. However, the country has yet to set net-zero carbon targets.

Egypt aims to become a leading green investment hub in the Middle East and Africa by fully transitioning to a sustainable green economy. The government launched the National Initiative for Smart Green Projects in 2022 to promote sustainability investment at the local urban level and vowed that 100% of government projects would be green by 2030.

The government’s targets are ambitious: the Vision 2030 developmental agenda aims for 42% of electricity generation and 60% of the total energy mix to come from renewables by 2030. As part of the Nexus of Water, Food, and Energy (NWFE) programme, it has dedicated $10 billion to adding 10 GW of renewable-energy capacity by the end of 2028. According to the International Renewable Energy Agency, Egypt needs investments worth $6.5 billion between 2014 and 2030 to achieve this goal.

The energy target is part of Egypt’s first National Climate Change Strategy 2050, which is designed to achieve several objectives, including establishing an advanced green-finance infrastructure. This includes a vision on supporting green banking and green credit, innovation in financing mechanisms, and encouraging greater private-sector participation and better compliance with guidelines of multilateral development banks for green finance.

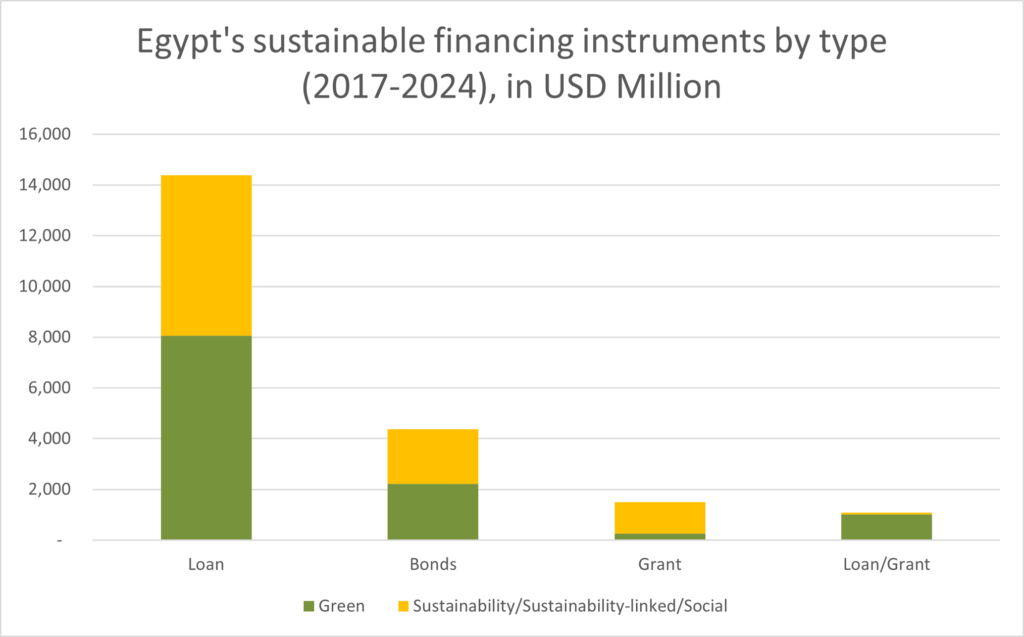

This agenda is reflected in Egypt’s three main domestic and external sustainable financing instruments: loans, grants and bonds, as Figure 1 shows.

Investments in Egypt’s renewable energy sector have increased in the past eight years, but still insufficient. The 2017 Renewable Energy Financing Framework established a partnership with the European Bank for Reconstruction and Development and the Green Climate Fund, raising $1 billion, including $250 million from the private sector. In the past five years, investments in renewable projects have injected billions of dollars into the Egyptian market through construction, financing and management contracts. On 8 April, Egypt and France finalized a $7.6 billion contract to establish a green hydrogen and ammonia production complex near Ras Shokeir on the Red Sea coast. This agreement encompasses the facility’s development, financing, construction and operation by Egyptian and French companies.

Despite the emphasis on turning the country into a formidable renewable-energy exporter, Egypt faces a significant financing gap. For example, the energy sector, including renewables, accounted for 1.47% of the sustainable loans and grants to Egypt in bilateral and multilateral agreements between 2017 and 2024, compared with 38.3% and 18.5% for the transport and agriculture sectors, respectively.

The energy-financing gap is primarily attributed to the dominance of profit-driven investments from the private sector, rather than on reliance on bilateral or multilateral sources. For instance, in 2023, only a year after its launch, the NWFE programme mobilized $2.18 billion of private-sector investments in renewable energy, which was followed by a slew of investments from different sources. Challenges, such as high public debt, fiscal constraints, a dated electricity grid and regulatory hurdles, also limit Egypt’s ability to finance new projects. This is starkly apparent in the fact that 89% its energy mix in 2024 came from oil and natural gas.

Social development is another top priority, reflected in three main financing instruments. Sustainability, sustainability-linked, and social loans, grants, and bonds have spiked since the launch in 2022 of the Sovereign Sustainable Financing Framework, which upgraded the old Green Financing Framework to focus more on social and governance issues beyond environmental concerns. Most of this funding has gone to social safety-net projects, such as the two flagship initiatives (the Takaful and Karama cash-transfer programmes for the most vulnerable and the localization of the Haya Karima sustainable development initiative), women’s empowerment and inclusion, encouraging greater participation by small and medium-sized enterprises, and sustainable infrastructure projects.

The broadening of the scope of sustainability financing aims to align spending with the government’s developmental agenda, as set out in Vision 2030. Furthermore, the banking sector, particularly government-owned banks that prioritize social-development investments, and corporations affiliated with the government, especially in the renewables sector, are the largest beneficiaries of external financing.

The collaboration with external partners in sustainable finance presents a long-term strategic opportunity for the government to prioritize accessing capital resources for social development, but this comes potentially at the expense of achieving environmental objectives. Egypt does not have a carbon-taxation system but an implicit carbon-pricing mechanism through the collection of the energy excise taxes. It has extremely low effective carbon rates (for social reasons) and a narrow focus on the road-transport sector, ignoring other big emitters such as the energy-generating and industry sectors.

Chinese, GCC and Western Financing

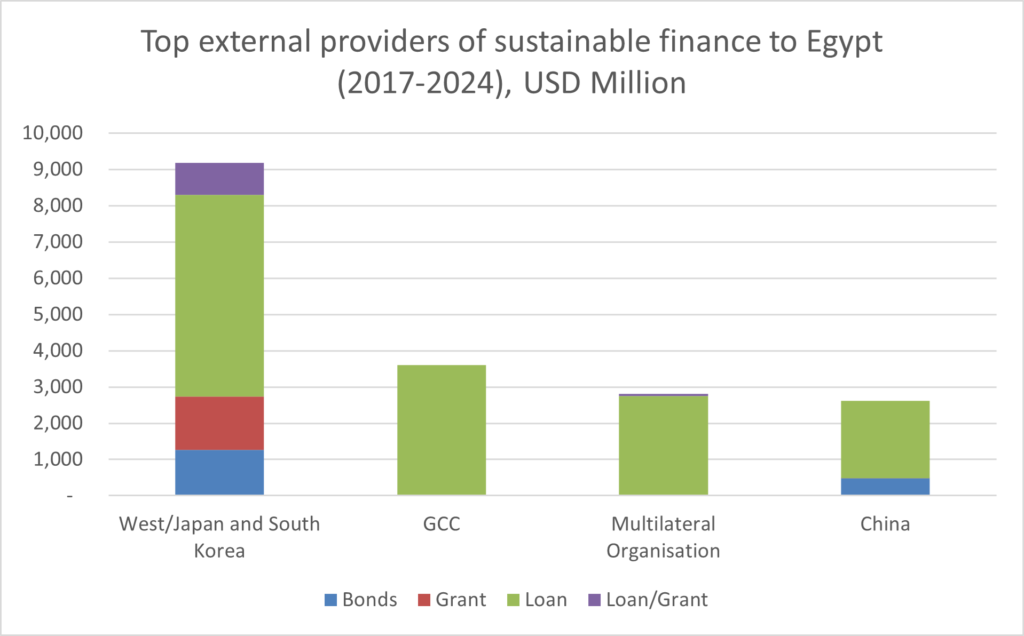

Financing for Egypt’s green financing initiatives is driven by direct investments from external states and multilateral organizations. The nature and the focus of these financing mechanisms varies by the region of origin, with a diverse range of financing mechanisms emerging from Western and East Asian countries. China and the members of the Gulf Cooperation Council (GCC) focus more on the issuance of repayment loans. The political agendas of external actors are reflected in these portfolios.

The data for 2017–24 shows differences in Chinese, GCC and Western approaches to sustainable financing in Egypt in terms of the type of financing, the platform used, the sectors and the purpose, whether mitigation or adaptation. Loans make up the biggest share of external financing, at 77%, while grants amount to 8.2%. Western entities lead in green and sustainable loans with 39.6%, ahead of the GCC countries with 25.6% and China with 15.2%. Western countries and organizations provided almost all of green and sustainable grants (98.8%). This reflects the more balanced Western approach to financing, while China and the GCC countries overwhelmingly concentrate on financial returns to themselves in the form of interest payments or return on direct investments. This explains the partnerships that GCC and Chinese companies and banks have targeted in Egypt’s renewables sector – particularly solar, wind and green hydrogen – in addition to renewables tech manufacturing and sustainable cities.

Support for non-sustainable financing projects continue to dwarf investment in sustainable projects. GCC sustainable financing amounted to $3.61 billion between 2017 and 2024, 19.8% of the total. By comparison, GCC bilateral agreements with Egypt on financial inflows in the form of oil and gas credits and central-bank deposits stood at $26 billion between 2017 and 2022. Direct investments play a central role in GCC financing strategy. The biggest example is the United Arab Emirates’ 2024 agreement to invest $35 billion to develop the Ras El Hekma peninsula on the Mediterranean Sea.

China focuses on high returns in specific areas, such as the Suez Canal Economic Zone or the New Administrative Capital near Cairo. Despite the favourable repayment conditions, its interest rates are usually higher than those of other lenders. For example, Egypt’s first renminbi-denominated sustainable Panda Bonds in 2023 was at a 3.51% rate compared to 1.5% for the yen-denominated Samurai Bonds in the same year.

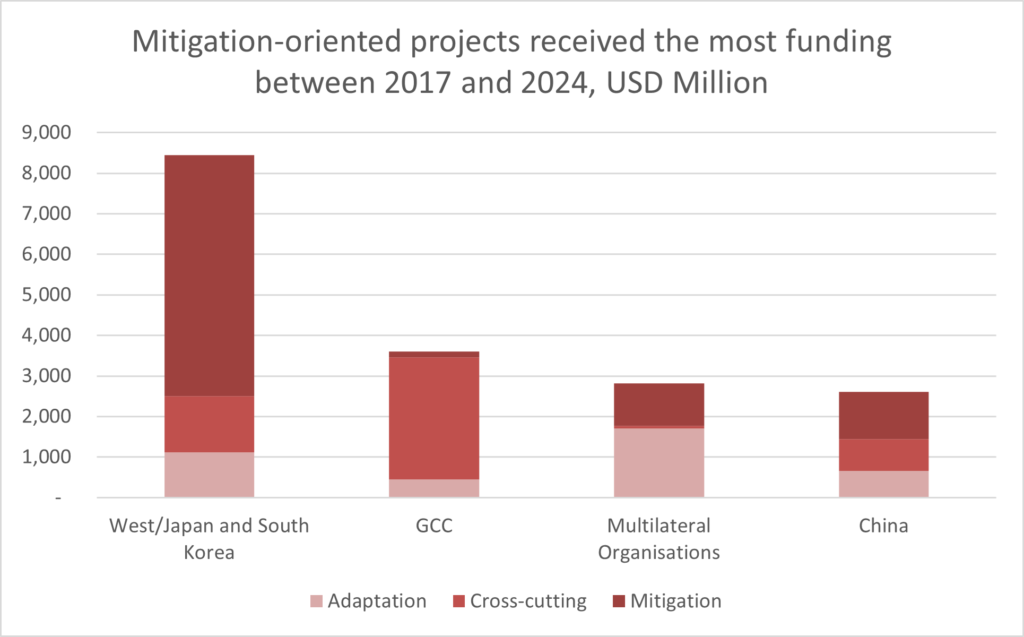

The breakdown of financed projects in figure 3 shows a Western focus on the long-term rehabilitation of Egypt’s water-management systems, agribusiness and rural development, while GCC funds provided assistance in securing the imports of grain and other essential agricultural products. Western and Chinese financing focused above all on the clean-transport sector, a high priority for Egypt’s government. The sector accounted for 60.2% of loans and grants from Western entities, Japan and South Korea, and 23.4% of the financing from China (Figure 3). GCC financing focused heavily on the agricultural and irrigation sector, addressing food security, another key government priority.

Western donors have also focused on various social programmes that align with their democratic values. These include initiatives promoting gender inclusivity, addressing irregular migration, supporting social safety nets, ensuring equality, and combating sexual harassment. By contrast, China’s financing is in line with its emphasis on the non-interference principle, which regards social and political initiatives as direct interference in other countries’ affairs.

In terms of priority sectors, Chinese and Western financing overwhelmingly focused on mitigation – largely because of clean-transport projects, while cross-cutting purposes dominated in the case of the GCC countries (Figure 4).

Egypt’s expressed desire to obtain membership in BRICS and other China-led organizations does not amount to a decisive ‘pivot to the East’ or reflect geopolitical intentions. Since 2020, Egypt has relied heavily for sustainable finance on multilateral organizations, which offered 60.4% of the total. Western multilateral entities – mainly the European Union, the European Bank for Reconstruction and Development and the European Investment Bank – provided of the multilateral contributions. Next were the World Bank at 25.6% and the regional multilateral development banks such as the Arab Fund for Economic and Social Development and the Islamic Development Bank, in which GCC countries play a pivotal role, at 25.4%. China-led multilateral development banks, mainly the Asian Infrastructure Investment Bank and BRICS’s New Development Bank, offered around 19%, a significant contribution given Egypt’s nascent membership in these organizations.

Consequently, Egypt’s agenda is better described as seeking diversification and a broader ranged of financing opportunities that support its developmental goals. This funding also shows rising trust in Egypt’s economy and commitment to sustainable growth.

How Egypt can build upon its progress: five priority areas

While Egypt has made significant progress, there are five priority areas where Egyptian policymakers could go further to accelerate Egypt’s green transition. First, Egypt should seek to reduce its heavy reliance on fossil fuels in energy generation by encouraging more private investments in the renewables sector. This could be done by modernizing the energy-generating sector, including by accelerating the upgrade of the electricity grid to allow for smoother transmission and distribution as well as to improve the storage infrastructure.

Second, adopting initiatives to align domestic financing policies with climate-related objectives would also support greater progress. For instance, there is an opportunity to narrow the scope of corporate income tax incentives to green projects, excluding businesses with high greenhouse-gas emissions. This would increase environment-related tax revenues without having to increase financial burdens on households.

Third, and more specifically, Egypt should first extend the tax on emissions in the transport sector to electricity generation and industrial sectors and design a carbon-tax system in order to incentivize a faster shift away from reliance on hydrocarbons.. A carbon tax system should include robust mechanisms for carbon pricing and pollution taxes and integrate it into the Tax Policies Document 2024-2030 that is under review. Egypt has already introduced a carbon-certificate mechanism as a basis for a voluntary carbon market.

Fourth, a green-product taxonomy system would enhance the tracking and reporting of public expenditure and private investments in specific environmental or climate goals to be better able to assess progress and identify opportunities for improvement. Egypt should utilize its partnerships with China and the EU (the leading taxonomy regulatory powers) to learn lessons from them in this field.

Finally, to unlock more financing opportunities from its foreign partners, Egypt should accelerate monetary and fiscal reforms to address the currency crisis and establish a more transparent financing mechanism for foreign lenders. It should also make progress in developing more vigorous systems that allow the private sector to benefit directly from available financing for green projects. Increasing financial incentives, such as subsidies or feed-in tariffs, for foreign investors in the clean-energy sector.

This article is part of a series that explores the green-finance initiatives of China and the GCC states in the Middle East and North Africa. Similarly to our articles China and the GCC, this one analyses Egypt’s approach to green finance as well as the Chinese, GCC and Western contributions to it, while outlining the hurdles that may face the country’s strategies. The analysis uses data from 2017 to 2024, with the exception of instances where data is unavailable due to low transparency or lacking due to the absence of projects and the nascent state of Egypt’s green-finance systems.