Green finance is critical to the efforts of Gulf countries to reduce their reliance on oil revenues. Analysis of their efforts to date reveals significant progress in the unveiling of green financing instruments. However, the data illustrates that fully realising these goals as part of a programme of sustainable growth is going to be dependent on navigating challenges associated with regulation, the absence of a green-product taxonomies system and ambiguous enforcement mechanisms.

For this to happen, the Gulf states will need to prioritise green finance by accelerating the decarbonisation process with a greater emphasis on environmental sustainability and expanding their plans beyond the realm of energy. A means of achieving this would be for each GCC country to consider creating a green investing body that focuses exclusively on project sustainable finance and management, while the development of a unified GCC approach should also be discussed to increase compatibility in the green transition across the region.

Green finance in the GCC

The six members of the Gulf Cooperation Council (GCC) – Bahrain, Kuwait, Qatar, Oman, Saudi Arabia and the United Arab Emirates – are major providers of green finance in the Middle East and North Africa. Green finance encompasses a range of financial activities, investments, and instruments designed to foster environmentally sustainable outcomes. This is particularly evident in initiatives focused on reducing carbon emissions, conserving natural resources, and advancing clean energy solutions and climate resilience.

GCC members’ engagement with green finance is driven by their national strategies to diversify their economies in order to reduce their reliance on oil revenues as the central growth driver. All GCC countries have net-zero carbon targets (2050 for Oman and the UAE, and 2060 for Bahrain, Kuwait and Saudi Arabia).

Financing the energy transition is a major factor in the GCC countries’ climate strategies, which set targets for energy generation from renewable sources, but with mixed results. For example, Oman and Saudi Arabia aim to have respectively 30% and 50% of their energy mix from renewable energy by 2030. The acceleration in economic diversification has turned green-finance instruments, such as sustainable loans and sukuk (the debt instrument compliant with Islamic laws), into mainstream strategies for governments, banks and corporations since 2017.

The GCC states’ green finance policies mirror the approach adopted by China. Economic and energy policies are transition-oriented, not disruptive, with a balanced approach that emphasises gradual phasing out of oil and gas while shifting to renewables.

Some GCC governments developed sustainable financing frameworks as regulatory foundations for green-finance policies. These include the UAE’s Sustainable Finance Framework (2021–2031), Oman’s Sustainable Finance Framework (2024) and Saudi Arabia Green Financing Framework (2024). These policy frameworks are important as they support GCC countries’ climate goals and demonstrate their government’s commitment to decarbonising their financial systems.

Systemic challenges remain that uncover the sustainable finance sector’s immaturity in the Gulf. For example, regulatory hurdles, such as disparities between GCC countries’ development and implementation of the new systems’ regulations, the absence of a green-product taxonomies system and ambiguous enforcement mechanisms characterize the GCC markets. These challenges hinder investors’ ability to assess the sustainability standards of investments, reduce the credibility of financial institutions and increase the risks of ‘greenwashing’. The absence of ESG-driven high-quality data is another major challenge for investors in tracking ESG compliance and performance reporting, and for making decisions accordingly. Other challenges include the high level of discrepancy in metrics and methodologies between jurisdictions and sectors (even within the GCC) and the scarcity of local sustainability skills and expertise.

However, these challenges did not prevent the introduction of green-finance instruments in the past four years. This shows the eagerness of GCC governments and private sectors to speed up the integration of sustainable financing in the mainstream finance ecosystem.

Financing instruments

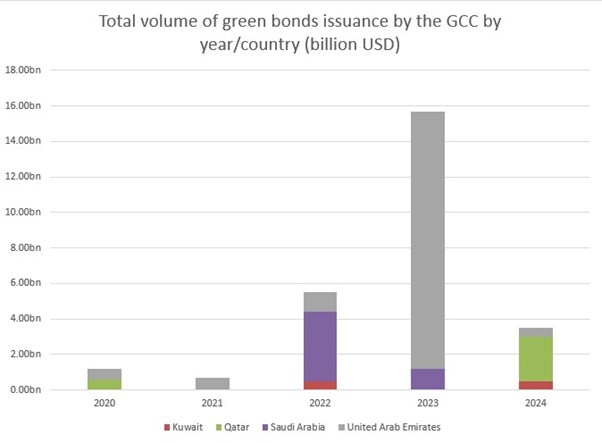

The United Arab Emirates leads the GCC in green-finance issuance in terms of outstanding bonds and sukuk. As Figure 1 shows, issuance of green bonds spiked very significantly to $15.66 billion in 2023 in these GCC countries due to the attention generated by the UAE hosting COP28 and to high interest rates. It then fell to $3.5 billion in 2024. While Saudi Arabia was the largest issuer in 2022 and the UAE in 2023, Qatar has also gradually increased its issuance to a high of $2.5 billion in 2024, demonstrating increasing awareness of the importance of green finance for the economic diversification plans across the GCC. However, this also shows disparities and inconsistency in the issuance volumes and the absence of a GCC unified approach in the adoption of financial sustainability.

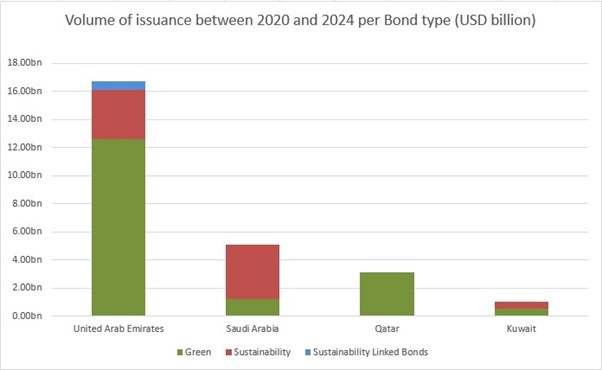

The composition of financial instruments reflects three main trends: a transitional focus on social stability and development over environmental concerns, the banks’ dominant position and oil’s central role in bankrolling the transition.

Green bonds are still prevalent as GCC economies try to reduce their reliance on oil and to speed up decarbonization. However, the issuance of sustainability bonds has increased notably due to the focus of Saudi and UAE sovereign and financial entities on financially balanced sustainability, including funding social projects (Figure 2). This is specifically related to the concentration of green finance in the banking sector, which is heavily exposed to socially oriented investments. Additionally, sustainable bonds provide flexibility and an emphasis on social development in the context of the GCC focus on gradual economic transformation underpinned by phased-transition policies that accommodate ongoing reliance on oil, often at the expense of environmental goals.

The data indicates that GCC contributions to green finance tend to decrease when oil prices are low or anticipated are expected to drop. This highlights a strong correlation between oil prices and the pace of transition within the GCC.

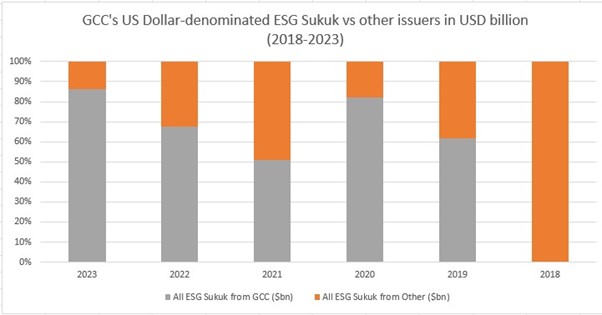

The GCC states dominate the global market of ESG sukuk. According to Fitch Ratings, sukuk amounted to 44% of the total GCC ESG debt capital market in 2024. Between 2018 and 2023, the GCC issued 68.2% of the dollar-denominated ESG sukuk globally, including green, sustainability and sustainability-linked sukuk (Figure 3).

The rise in sustainability sukuk continued in 2024 in the GCC despite the decline in ESG bonds. The sukuk contribution to green finance in these countries is likely to increase in line with the shift in their green-finance strategies and focus on Islamic ESG instruments in the last few years. The rise of sukuk is important due to several factors, including alignment with Islamic principles, investor demand in Islamic countries, flexible use of proceeds, the social-development dimension and the congruence with Western investors’ environmental objectives. This may unveil a GCC collective perception towards sukuk as an all-rounder financial instrument that meets a broad range of diverse developmental objects beyond environmental concerns by integrating Islamic sukuks into the GCC’s economic diversification plans.

GCC and Chinese green finance in MENA

Data shows a high level of compatibility in the GCC and China’s approaches to MENA’s financing, indicating similar strategies and objectives.

Green financing from the GCC countries and China rose significantly between 2021 and 2023, but declined in 2024 despite the increase in the total funding flows. In the GCC, this is due to low oil prices, which are forecasted to decline further in 2025 and 2026 to $65–$70 a barrel, creating additional constraints for national budgets. Additionally, GCC governments and sovereign wealth funds are focusing on domestic investments to support economic diversification, and they aim to secure preferential access to acquire public or private assets as investments abroad.

China has reduced its contribution to global green finance due to its stagnant economy, restructuring of development finance towards high selectivity and de-risking, and the debt bubble from lending to countries in economic crisis. This shift aligns with the recommendations from the second BRI Forum in 2019, which advocated for reducing high-risk lending and a renewed focus on smaller, more sustainable projects.

There is also high correlation on the objectives: both sides prioritise profitability, focus on enhancing energy security, therefore paying more attention to mitigation over adaptation, and encourage a gradual decarbonisation path. They also prioritise the same recipients (mainly Egypt) in terms of fund volumes, demonstrating the emphasis on bilateral ties and geopolitical objectives.

Development-finance flows from different sources (including bilateral, private and multilateral platforms) into MENA’s low- and middle-income countries amounted to $457.3 billion between 2013 and 2024. This includes loans, bonds, equity and other forms of financing. There was a significant increase in the number of financing agreements in 2021 due to COVID-19’s impact on developing countries’ public finance and debt, the global emphasis on environmental transition and the rise in the contributions from green finance.

According to the Organisation for Economic Co-operation and Development (OECD), the UAE was the largest green-finance provider in MENA’s low- and middle-income countries until 2021, followed by Saudi Arabia. The majority of financing was dedicated to mitigation, reflecting GCC lenders’ focus on investing in the energy sector. The top recipients of GCC green finance were Egypt, Jordan, Morocco and the Palestinian Territories. Most of the mitigation funds went to Egypt and Morocco, while adaptation-oriented projects were more concentrated in Jordan and the Palestinian Territories. In the same period, Egypt, Iran, Iraq and Turkey received most of China’s green finance in the region.

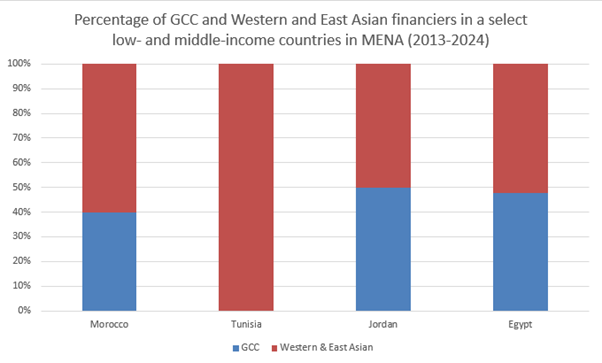

A comparison between GCC green finance and Western project finance in selected MENA countries also shows a high degree of convergence when it comes to recipient countries, the number of deals and the targeted sector. Between 2013 and 2024, Egypt, Jordan, Morocco and Tunisia received most of the green-project financing, at from Western, East Asian (excluding China) and GCC countries as well as China. The majority of the projects were partnerships and received financing from different sources. Qatar, Saudi Arabia and the UAE participated in the financing of 49% of the projects through partnerships, while Western and East Asian countries partnered with other countries, including the GCC ones, for 56% of them (Figure 4). Energy and power was the main sector targeted (89%).

The same pattern can be observed when comparing the flows from the GCC countries and China with both sides targeting the same sectors between 2013 and 2024, the top three being energy, government agencies and financial institutions. This was motivated by similar objectives, including enhancing bilateral relations through financial cooperation as part of MENA countries’ diversification and targeting specific projects owned or promoted by the government in countries where the GCC and Chinese banking sectors play a key role. For example, both sides focus on boosting MENA’s energy transition, mirroring their domestic policies by dedicating funds to energy projects – particularly solar power, wind farms, hydrogen production, electric vehicles and electricity production. Energy security is also a major driver behind this approach as the GCC countries, principally Saudi Arabia and the UAE, try to maintain their positions as major energy players, while China has the ambition and resources to dominate the future renewable energy markets. The OECD data shows that 55.6% of GCC green finance was dedicated to mitigation and 44.4% for adaptation.

There is insufficient data to assess properly the GCC countries’ participation in multilateral organizations in this field. However, the OECD data suggests they prefer bilateral deals and hesitate to dedicate large funds to multilateral development banks and international financial institutions. Qatar, Kuwait, Saudi Arabia and the UAE dedicated only $285 million to multilateral green-finance initiatives. Most of this, $224 million, came from Saudi Arabia, with Kuwait next with $48 million. The overall picture is consistent with the GCC countries’ economic diplomacy, which focuses on pursuing their national financial benefits or geostrategic objectives through bilateral aid, loans and other financing tools.

Conclusion

The data indicates that GCC countries’ green-finance ecosystems are underdeveloped. This is because incentives designed to facilitate the green transition within the financial system can occasionally clash with the government’s strategic goals related to social development and economic growth.

To reach their objectives, the GCC countries need more efforts to develop their green finance ecosystems to not miss the $2 trillion in economic growth and more than a million new jobs as predicted by the PwC’s Strategy&. This will require a shift in the mindset from seeing green finance only as an opportunity to also perceive it as a priority.

The GCC governments should accelerate the decarbonisation process by focusing more on environmental sustainability by making it a main pillar in its energy transition strategies and financial planning, including debt instruments. A means of achieving this would be for each GCC country to consider creating a green investing body that focuses exclusively on project sustainable finance and management, such as a green sovereign wealth fund. A unified GCC approach should also be discussed to increase compatibility in the green transition across the region. Finally, there should be more focus on themes beyond energy, infrastructure and water management to include sustainable agriculture, sustainable tourism and circular economy by utilizing green finance as the main driver beyond this diversification.

This article is part of a series that explores the green-finance initiatives of China and the GCC states in these countries. Similar to our initial article on China, this one analyses the GCC approach to green finance and compares it with that of China, using data from 2013 to 2024, while outlining the hurdles that may face their green finance strategies. Exceptions are made for instances where data is only available until 2021 due to low transparency and the limited availability of official data, or where data is lacking due to the absence of projects and the nascent state of the GCC states’ green financial systems.